Commentary

The demands of the Kremlin’s war in Ukraine, demographic problems, and public hostility toward Central Asians mean Russia does not have enough workers.

Salavat Abylkalikov

{

"authors": [

"Mikhail Korostikov"

],

"type": "commentary",

"blog": "Carnegie Politika",

"centerAffiliationAll": "",

"centers": [

"Carnegie Endowment for International Peace",

"Carnegie Russia Eurasia Center"

],

"collections": [

"The Iran War’s Global Reach"

],

"englishNewsletterAll": "",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Russia Eurasia Center",

"programAffiliation": "",

"regions": [

"Russia",

"China",

"Iran"

],

"topics": [

"Foreign Policy"

]

}

Source: Getty

The interventions in Iran and Venezuela are in keeping with Trump’s strategy of containing China, but also strengthen Russia’s position.

The war launched against Iran by the United States and Israel is escalating rapidly, and how events will unfold is hard to predict. But what is already certain is that one of the main losers of the hostilities will be China. In 2025, about one-fifth of China’s oil imports came from Iran and Venezuela—which also recently found itself on the receiving end of a U.S. intervention. Now that those supplies are compromised, the primary beneficiary is Russia, which is ready to increase oil exports to China.

There are no official statistics on China’s dependence on Iranian and Venezuelan oil, since most of the deliveries were conducted clandestinely due to Western sanctions. However, indirect estimates indicate that the two countries accounted for about 17–18 percent of China’s total oil imports as of the end of 2025.

Due to those same sanctions, both Venezuela and Iran provided China with oil at a significant discount. The business model of many independent Chinese refineries in the south of the country was built on refining this heavy and relatively cheap crude. To preserve these flows, a complex infrastructure for evading sanctions was built, from the use of a shadow fleet to ship-to-ship cargo transfers in international waters and the subsequent legalization of that cargo through ports in Malaysia, the UAE, and Oman.

Now Iranian supplies could face the same fate that has befallen Venezuelan supplies in the last two months. In 2025, Venezuela’s total oil exports amounted to approximately 0.9 million barrels per day, over 80 percent of which went to China. A significant portion of that was used to pay off Venezuela’s debt to China. The main buyers were small Chinese refineries accustomed to handling heavy, high-sulfur, and inexpensive crude.

From the U.S. intervention at the start of the year, which resulted in U.S. forces capturing Venezuelan President Nicolas Maduro, new shipments have all but stopped, and Chinese cargoes are either being returned or diverted. Washington claims that all Venezuelan exports must now go “via legal channels,” and is reselling some of the Venezuelan oil it purchased—including to China.

Independent Chinese refineries are preparing to switch to Iranian, Russian, and Canadian heavy grades in the second quarter. But now that the future of Iranian supplies is also uncertain, that will become more difficult.

Even a complete halt to Iranian and Venezuelan exports won’t lead to an immediate crisis in China, but it will torpedo the pricing model on which entire segments of the Chinese economy are built, such as the aforementioned small refineries, which make up about a quarter of all Chinese oil refining.

China can replace the lost volumes by increasing imports from Saudi Arabia, Iraq, Russia, Brazil, and the United States, but they will be more expensive and often less convenient in terms of their quality, which will automatically mean a squeeze on margins, higher domestic prices, and the reduced competitiveness of energy-intensive exports.

There are also some less immediately visible losses in the form of China’s long-term investments in the two countries. The total volume of Chinese loans and investment in Venezuela is estimated at $50–60 billion, of which about $10–15 billion is in loans secured by oil supplies. This means that a significant proportion of the oil on which Beijing had been counting as debt repayment will now either never reach China or is being resold with U.S. involvement.

The corresponding figures for Iran are significantly lower. Chinese investment in Iran from 2005 to 2025 amounted to just $4.7 billion. The main obstacle to further investment is Western sanctions: Chinese companies don’t want to take the risk. To make matters worse, instead of protecting against U.S. intervention, Chinese investments actually increase its likelihood, given the current U.S. administration’s unconcealed ambition to contain China.

Of China’s top ten oil suppliers, two have been eliminated, and another five (Saudi Arabia, Oman, the UAE, Kuwait, and Malaysia) are close U.S. allies. The remaining three are Russia, Iraq, and Brazil. Trump is looking for an excuse to have a showdown with Brazil, but its share of Chinese imports is small: around 4–5 percent.

Iraq has been supplying about 10 percent of China’s total oil imports in recent years. By 2023, Chinese investment Iraq had reached $34 billion, nearly 90 percent of which was in the energy sector. In 2025, Chinese companies owned 7.3 percent of the shares in Iraq’s licensed oil and gas projects, compared with 1.8 percent owned by U.S. companies. Given that the United States has retained a strong influence over Iraq’s security sphere since the 2003 invasion, Trump could easily argue that thousands of American soldiers died “liberating Iraq from the tyranny of Saddam Hussein,” accuse Baghdad of being “ungrateful,” and launch a pressure campaign demanding that it reconsider its cooperation with Beijing.

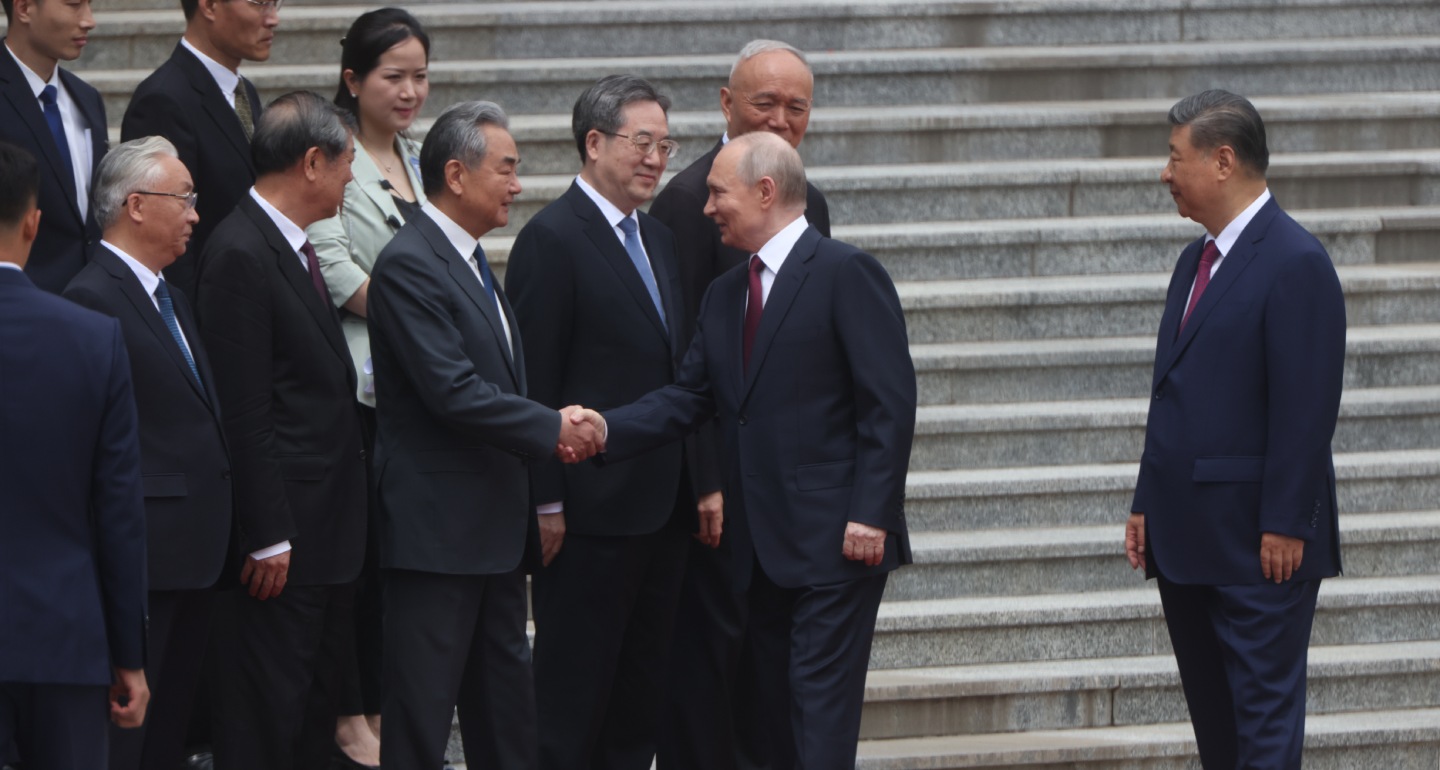

It was Russia, however, that had by 2025 become the undisputed leader in Chinese oil imports, accounting for 17.5 percent. Accordingly, Moscow is emerging as one of the main beneficiaries of Trump’s Venezuelan and Iranian interventions. It could well redirect some of its oil exports from India to China, thereby simultaneously easing American pressure on New Delhi and supporting Beijing. This redistribution has already begun following the decline in Venezuelan supplies, and is now likely to accelerate.

Trump’s interventions give Moscow an opportunity to reaffirm the key argument behind the Russian-Chinese rapprochement: that maritime routes for supplying resources to China could be cut off at any moment by the United States, so the only reliable option is pipelines and roads from Russia. The Power of Siberia 2 gas pipeline project, which was finally agreed at the political level in September 2025, could be accelerated. It’s also possible that other infrastructure initiatives will now receive greater attention, such as a joint program between Russian Railways and Mongolian Railways that would increase the annual throughput capacity of the corridor through Mongolia to 50 million tons by 2030.

If the Trump administration truly intends to pry away China’s key partners one by one, then every such victory over a resource supplier to China will strengthen the position of Russia, since it is capable of providing commercial quantities of practically any resource. Back in less turbulent times, Beijing could afford to diversify its supplies, but faced with a growing confrontation, there are more and more incentives to choose the safest option: i.e., Russia, which not only possesses abundant reserves of a wide variety of resources, but is also able to guarantee supply stability through its geography and nuclear umbrella.

Mikhail Korostikov

Sinologist

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

The demands of the Kremlin’s war in Ukraine, demographic problems, and public hostility toward Central Asians mean Russia does not have enough workers.

Salavat Abylkalikov

Minsk’s faith in the future of its larger neighbor’s economy is fading as Belarusian firms in Russia see record losses.

Olga Loiko

With no key agreement signed on the Power of Siberia 2 gas pipeline, there is a risk that the window of opportunity for Russia will close if Chinese power generation becomes so green that new gas sources are no longer of any interest to Beijing.

Alexander Gabuev

Though Orban is gone, Putin can still count on some like-minded individuals in Central and Eastern Europe. However, they will seek to avoid open confrontation with EU institutions over Ukraine and their ties with Moscow.

Dimitar Bechev

The truth is that Japan’s government is seeking a degree of reengagement but at a vastly reduced level than under Abe. Most significantly, Japan has shown no willingness to ease sanctions.

James D.J. Brown